The financial services sector also faces higher attribution fraud exposure. Forty percent of surveyed companies reported being targeted by fraud in 2025, with financial services organizations experiencing disproportionate exposure, according to Sumsub’s Identity Fraud Report, At $50 to $200+ per qualified user acquisition in competitive markets, even a 10% fraud rate translates to hundreds of thousands in wasted spend annually.

Attribution fraud hits financial technology companies harder than most verticals. Your customers carry exceptionally high lifetime values (LTVs): a single banking app user who maintains an account for years represents thousands of dollars in revenue. That value is exactly what makes fintech a target. Higher user values drive higher costs per action (CPAs), and bigger CPAs mean bigger payouts per stolen conversion. Fraudsters collect the full CPA for every fraudulent claim they make

Attribution fraud creates compliance problems unique to fintech marketers by corrupting marketing data and impacting the source-of-truth records regulators expect.

What is attribution fraud, and why are financial technology companies prime targets?

Attribution fraud is the deliberate manipulation of attribution data to assign credit for user conversions to a publisher or affiliate that didn’t have a role in generating it. Fraudsters exploit tracking mechanisms to make it appear a source influenced an install, sign-up, or transactions they didn’t drive.. It corrupts the performance data leading marketers to cut channels that are working and scale ones that aren’t.

Financial services customers have exceptionally high lifetime values, which makes fintech acquisition funnels a target for fraudsters. A single stolen conversion can yield outsized payouts.

Last-click hijacking through affiliate and sub-affiliate traffic

Affiliate and sub-affiliate traffic is a frequent source of attribution fraud in fintech. Fraudulent affiliates monitor user behavior and inject themselves into the conversion path immediately before a user completes a signup or transaction, claiming credit for conversions they didn’t drive.

A user discovers your fintech app through a brand campaign or organic search, downloads it, and begins account creation. Just before they complete registration, a malicious affiliate fires a click that appears to be the “last touch” before conversion. Your attribution system credits that affiliate, and you pay a commission for a user who was already committed to signing up.

Common last-click hijacking tactics include:

- Click spamming: Firing a high volume of clicks so one eventually lines up with an organic install the affiliate didn’t drive, often showing up as an unusually long click-to-install time

- Cookie stuffing: Dropping tracking cookies without genuine engagement

- Toolbar and browser extension manipulation: Firing affiliate clicks regardless of coupon use

- URL parameter injection: Appending affiliate parameters to organic URLs

- Redirect chains: Inserting fraudulent touches before users reach your landing page

These conversions appear legitimate in your reporting because the users are real and the installs are genuine, making it difficult to distinguish earned from stolen attribution without sophisticated detection.

Click injection and SDK manipulation in mobile app acquisition

Mobile app acquisition fraud has evolved far beyond simple bot traffic. Click injection exploits Android’s broadcast listeners to fire fraudulent clicks after a legitimate install has begun but before the user opens the app for the first time. A compromised app already on the user’s device detects the install in progress, then fires a fake click designed to win last-touch attribution credit for an acquisition another channel actually drove.

Software development kit (SDK) manipulation takes this threat further. Fraudsters create modified versions of legitimate attribution SDKs or inject code that alters how attribution data is collected. These manipulated SDKs can generate fake install events, modify device identifiers to simulate new users, alter timestamps to win attribution credit, and bypass standard fraud detection mechanisms.

UTM parameter spoofing and redirect chain exploitation

UTM parameter spoofing is difficult to detect because the user journey appears technically valid, with a real click, a real user, and a real conversion. Fraudsters intercept legitimate user journeys through redirect chains, strip your original UTM parameters, and replace them with fraudulent ones that credit a different source. The user completes their account opening or loan application. The fraudster collects the payout for a conversion they never influenced.

This distorts your channel performance data and pushes you to cut budget from higher-performing channels.

Detecting attribution fraud in fintech customer acquisition

Spotting attribution fraud requires statistical vigilance, behavioral analysis, and technical safeguards working together.

Analyze performance anomalies and user behavior patterns

Three patterns indicate attribution fraud:

Sudden performance spikes that don’t match user quality. A traffic source delivering 300% more conversions overnight without a corresponding campaign change indicates fraud. Legitimate growth follows predictable patterns tied to marketing activities. Fraudulent traffic appears as unexplained surges concentrated around specific partners or channels.

Time-to-conversion patterns. Genuine fintech users research financial products before converting. They compare rates, read reviews, and evaluate security features. Fraudulent conversions often show unrealistic fast time-to-install or time-to-registration metrics, frequently completing within seconds of the attributed click.

Post-install engagement. Fraudulent installs rarely progress beyond the initial app open. Unlike real users, fraudsters never complete KYC verification, link bank accounts, or make transactions — so high install volumes from a specific source paired with near-zero Day 7 or Day 30 retention is a reliable signal that the attribution is being gamed. These users generate no revenue and leave no meaningful behavioral trace.

Identify server-side event discrepancies

Server-side event discrepancies reveal one of the most telling signatures of attribution fraud: the gap between what your client-side tracking reports and what your server actually records. Fraudsters typically focus on client-side signals like clicks and impressions. They are unable to fabricate downstream events that happen on your servers, like account creations, KYC completions, first deposits, or loan applications.

Monitor for:

- Conversion rate anomalies, like 500 attributed installs but only 12 account registrations signals potential click injection

- Suspiciously uniform time-to-conversion timing

- Event sequence violations, where events fire out of order or skip mandatory steps

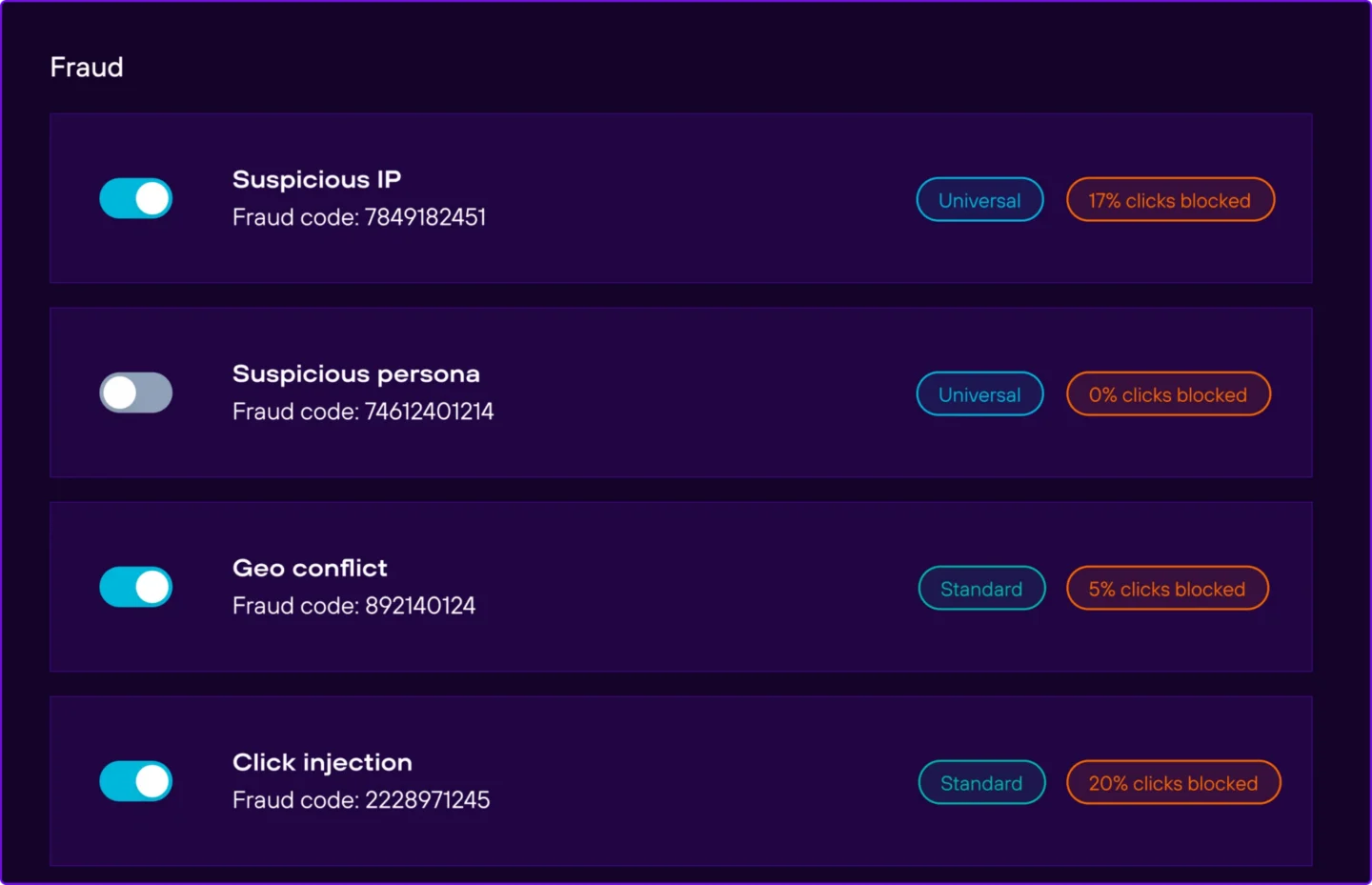

The Branch fraud detection platform blocks fraudsters in real time. It applies configurable rules, including suspicious conversion times, device conflicts, geo conflicts, suspicious devices. Branch catches fraudulent attributions before they distort your dashboard or your spend decisions.

Implement measurement design controls

Measurement design controls make it structurally difficult for fraudsters to manipulate your data. Three controls deliver the most protection:

Realistic attribution windows. Set attribution windows to reflect realistic user behavior in fintech. Financial app users typically need 24–72 hours to review terms, complete identity verification, and make informed decisions. Tighter windows reduce the time click spammers can claim credit for organic conversions. Pair attribution windows with suspicious conversion time rules that flag installs occurring within seconds of a click filters out fraud at both ends of the timing range.

Clear attribution logic hierarchies. Prioritize deterministic matching over probabilistic methods, favoring device-level matching and authenticated user data over easily spoofed signals like IP addresses.

Conversion validation rules. Require meaningful in-app actions (account creation, KYC submission, or initial deposit) before crediting high-value events. Multi-step validation eliminates the opportunity for fraudsters to claim credit for conversions.

Establish partner governance and contract requirements

Marketing partners can be your strongest allies in fighting attribution fraud. Embed anti-fraud measures into every partner contract:

- Prohibit specific tactics and specify that partners must not engage in click injection, install hijacking, or any form of attribution manipulation.

- Define performance benchmarks that trigger fraud reviews.

- Require granular reporting on traffic sources and user acquisition methods.

- Build in financial consequences for confirmed fraud, including clawback provisions and tiered penalty systems that make fraud financially unviable.

Deploy technical validation and bot filtering

Technical validation and bot filtering identify fraudulent attacks that measurement controls and partner governance do not catch.

Device fingerprinting and behavioral analysis distinguish legitimate users from bots, examining device characteristics, network patterns, interaction timing, and behavioral sequences.

Server-side validation checks confirm that install timestamps align with click time stamps, device identifiers match across events, and IP addresses correspond to expected geographic locations.

Real-time fraud scoring blocks suspicious traffic immediately rather than discovering fraud weeks later during monthly reporting.

For fintech campaigns where user acquisition costs are high and compliance requirements are strict, set conservative thresholds: it’s better to lose a few edge-case attributions than to pay for fraudulent conversions.

Building a multi-layer attribution fraud prevention framework

A durable fraud prevention framework runs in five layers:

- Layer 1: Technical validation and filtering. Implement device fingerprinting, bot filtering, and IP reputation scoring to prevent fraudulent traffic from entering your attribution data.

- Layer 2: Measurement design controls. Set realistic attribution windows, implement probabilistic matching alongside deterministic methods, and establish clear rules for crediting conversions across multiple touchpoints.

- Layer 3: Partner governance and oversight. Establish performance baselines for each partner, require transparency into their traffic sources, and build penalty clauses for verified fraud into every contract. Regular audits identify which relationships deliver genuine value.

- Layer 4: Continuous monitoring and analysis. Monitor conversion velocity, user engagement depth, and post-install behavior to spot anomalies as they emerge.

- Layer 5: Compliance integration. Attribution fraud is a compliance risk. Fraud prevention framework must align with KYC requirements, anti-money laundering protocols, and regulatory reporting standards.

Common questions about attribution fraud in fintech

Attribution fraud targets the credit assignment process for conversions, rather than fabricating fake users or clicks. Click fraud generates fake clicks to drain ad budgets, whereas install fraud creates fake app downloads. Fraud manipulates legitimate user journeys to steal recognition for conversions that would have happened anyway. The users are real; they just didn’t come from the source claiming credit.

Attribution fraud exploits the complexity of multitouch attribution. Its financial impact compounds over time by corrupting your entire marketing strategy and misallocating future budgets.

Pause payments to suspicious partners immediately and begin a forensic audit of your attribution data. Pull granular data for the past 30–90 days and examine high conversion rates, abnormal time-to-install patterns, geographic mismatches between click and install locations, or clusters of installs occurring within seconds of each other.

- Convene your fraud response team, including marketing operations, legal, compliance, and your attribution platform provider.

- Tighten your attribution windows.

- Enable server-side validation for high-value events.

- Activate fraud filtering functionality.

- Audit your entire partner ecosystem.

Protect your fintech marketing investments from attribution fraud

Fintech marketers who implement comprehensive fraud prevention frameworks gain clearer performance insights, stronger partner relationships, and better data integrity. But only if the attribution platform underneath can keep up. Every fraudulent conversion that slips through wastes budget, distorts campaign data, and creates potential compliance exposure.

Branch delivers fraud protection built for the complexity of financial services marketing: real-time fraud monitoring, an open-source SDK your security team can audit line by line, and cross-channel visibility across mobile and web. Transparent reporting makes it straightforward to audit partner performance, validate campaign results, and demonstrate measurement integrity to stakeholders and regulators.

Work with Branch to lock down attribution across every fintech acquisition channel. The conversions you pay for are the conversions you earned.